The WIFO study commissioned by the Chamber of Labour simulates – for the first time for Austria – the effects of

the CCCTB on Austrian corporate tax revenues. The harmonisation of the tax base as well as consolidation and formula apportionment

are analysed separately. In addition, WIFO tax experts Simon Loretz and Margit Schratzenstaller addressed the question of

how the CCCTB would affect tax competition in the EU.

The study shows that the expected budgetary effects of a harmonisation of the tax base (CCTB) for Austria are low. The proposed

EU directive contains provisions that would broaden the tax base and thus lead to higher tax revenues (e.g. by limiting the

deduction of interest payments) as well as provisions that would reduce the tax base (e.g. by more flexible discounting of

provisions). In addition, there are rules which are very similar to the current Austrian rules (e.g. depreciation of fixed

assets). Overall, it can be assumed that corporate income tax revenue will change moderately only as a result of tax base

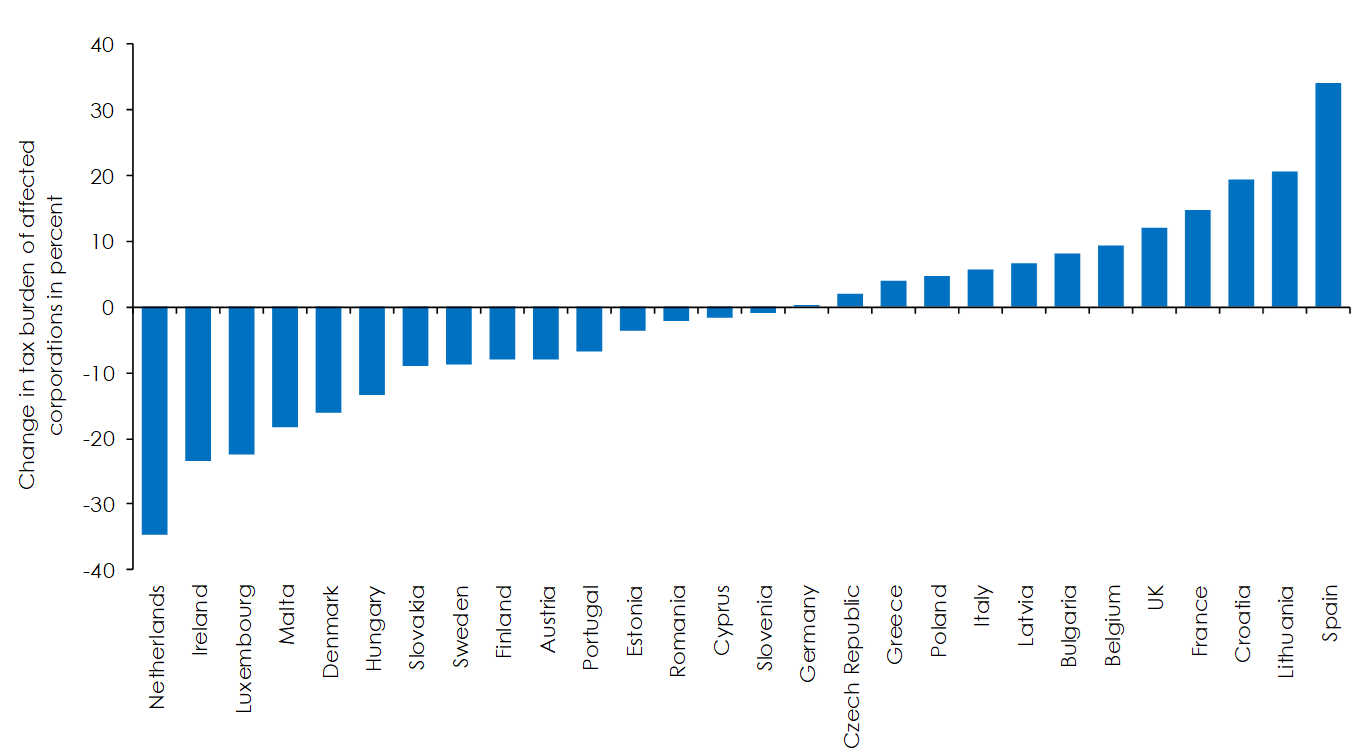

harmonisation.The consolidation of profits (CCCTB) in the second step would result in slight tax losses. This is due to the fact that Austria

has so far benefited more from profit shifting within the EU (in contrast to profit shifting with the rest of the world).

Also, the apportionment factors are relevant. While an apportionment of consolidated profits according to the number of employees

would favour Eastern European countries in particular, Austria would benefit from using the wage bill (including employers’

social security contributions) as apportionment factor.

Figure: Impact of consolidation and formula apportionment

Source: WIFO.

The resulting tax changes have an impact on firms and their decisions. On the one hand, firms’ tax planning options would

be restricted, while on the other hand they would benefit from a significant reduction of the administrative burden through

the harmonisation of the tax base. At present, multinational companies active in the EU have to comply with up to 28 different

national tax laws. According to the European Commission's proposals, uniform consolidation rules would apply in future. Only

one tax authority would be responsible for tax enforcement (one-stop shop).

Another important finding of the study is that the introduction of the CCCTB would not put an end to tax competition in the

EU but would rather change it. In the new system, corporate profits can no longer be shifted to low tax countries, but are

taxed (according to the apportionment formula) at the place of value added creation. To exploit tax rate differentials, firms

must shift real activities such as factories, distribution companies, supply chains, etc., which would be associated with

higher costs compared to the shifting of profits. Tax competition would therefore become less attractive.

At the same time, the CCCTB also makes corporate taxation more transparent and could thus intensify tax competition. Because

of the different rules for determining profits, it has so far been practically impossible for firms to precisely determine

and compare the effective tax burden at individual locations. This will no longer be a problem in the future. With effective

tax burdens becoming fully transparent, pressure on nominal tax rates will increase. In addition, nominal tax rates will remain

the only competition parameter. Overall, therefore, it can be expected that the CCCTB will increase downward pressure on nominal

corporate income tax rates and thereby boost tax competition in the EU.

To the blog post at Arbeit&Wirtschaft

and Margit Schratzenstaller (centre) with Dominik Bernhofer (Chamber of Labour) – © Chamber of Labour.")