"Unfavourable supply shocks are increasingly dampening economic momentum and intensifying upward pressure on prices," says Christian Glocker, author of the current WIFO Business Cycle Report.

The global economy continues to grow, but at a declining pace. The slowdown in growth – a consequence of persistently high inflation, disrupted supply chains, the continuing COVID-19 pandemic and the Ukraine war – is also shaping the economic path in Austria. Although the domestic economy is experiencing headwinds in the form of weaker foreign demand as a result, this is being countered by the extensive easing of official COVID-19 measures. Against this backdrop, GDP in Austria grew by 1.5 percent quarter-on-quarter in first quarter of 2022, after contracting in the fourth quarter of 2021. On the supply side, all sectors contributed to the expansion, while on the demand side it was mainly the expansion of gross fixed capital formation, private household consumption and exports.

However, leading indicators point to a slowdown in economic activity. The WIFO Business Climate Index in May was significantly lower than in the previous month but remained positive and above the long-term average. The UniCredit Bank Austria Purchasing Managers' Index also declined in May compared to the previous month. Low consumer confidence also clouded the outlook.

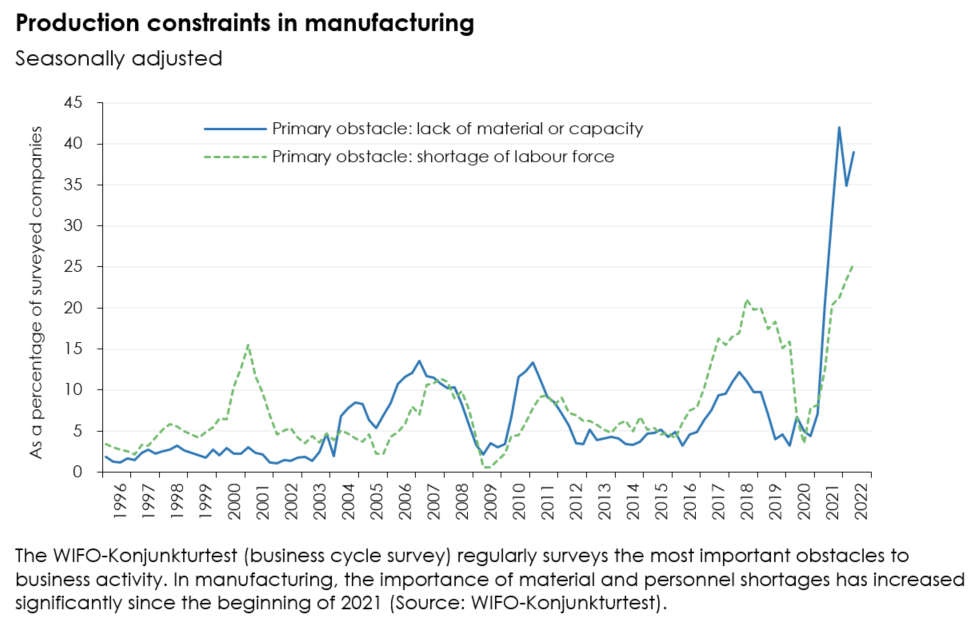

The overall economic expansion is clearly leaving its mark on the labour market. Employment continues to grow strongly (May: expected +2.8 percent year-on-year), while unemployment is falling. Employment remains higher than in the winter of 2020 before the outbreak of the COVID-19 pandemic, and unemployment is significantly lower. However, with the upswing, the labour shortages of the pre-crisis years have returned: according to the WIFO-Konjunkturtest (business cycle survey), staff shortages are a major obstacle to economic activity, and to an even greater extent than before the pandemic.

Price inflation remains high. The double-digit growth rates in producer prices observed for some time are increasingly reflected in consumer prices. The latter again increased significantly in April (+7.2 percent year-on-year, flash estimate for May +8 percent; according to CPI).