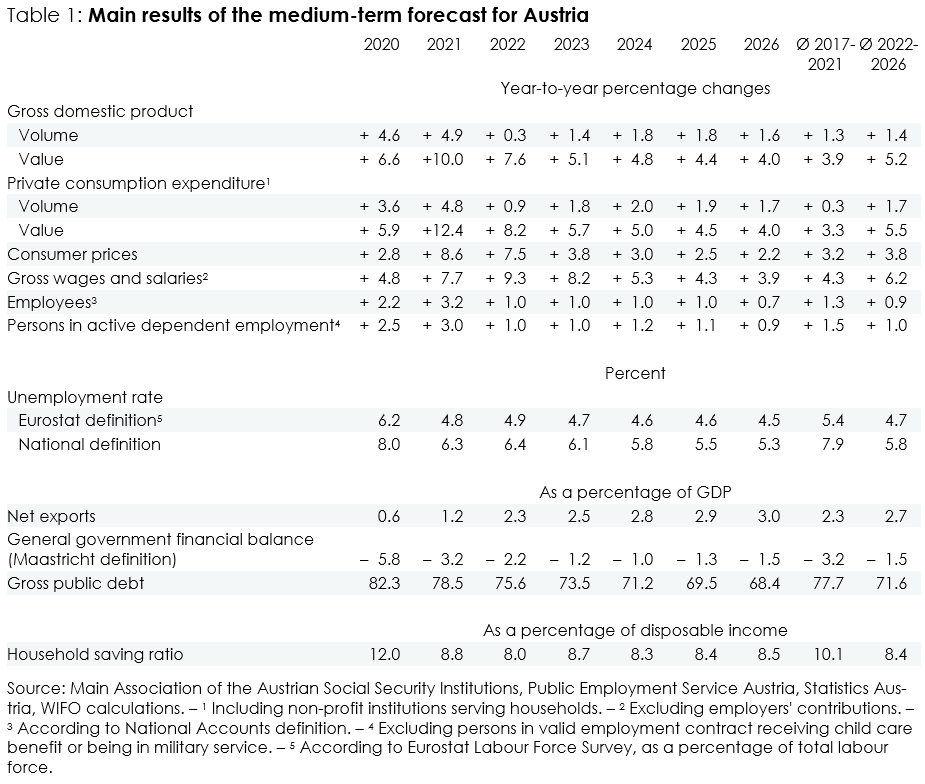

Gradual Recovery after Stagflation

In 2023, Austria's economy is experiencing a stagflation phase (GDP +0.3 percent, inflation +7.5 percent), as high energy prices reduce production possibilities and competitiveness, especially of globally operating energy-intensive companies. The resulting strong inflation leads, ceteris paribus, to a loss of purchasing power, which dampens consumption. The negative consequences of inflation are mitigated by (mainly permanent) income-supporting fiscal policy measures. The shortfall in the supply of Russian energy (especially natural gas) primarily affects the European economies and thus a large part of Austria's most important trading partners, with exports suffering as a result. Although European wholesale prices for gas and electricity have fallen again since October 2022, the low price level of 2020-21 will not be reached again in the forecast period and will remain above the price level in the USA and other non-European industrialised countries. The rise in energy prices will therefore continue to impact in particular energy-intensive industry also over the medium term.

In addition to the direct effects, the energy price hike also had an indirect impact in 2022, through (in some areas disproportionate) pass-throughs of higher energy costs to all prices of other goods and services. Amplified by supply bottlenecks (supply chains and capacity constraints) in the face of high (consumer) demand for goods, this led to the highest inflation rate since the 1970s in 2022 (+8.6 percent). With household energy prices still rising in the first half of the year and higher wage costs due to inflation, the rate of inflation is expected to reach 7.5 percent in 2023. With the easing of supply chains disruptions and the decline in household rates for gas and electricity, the inflation rate should fall to 3.8 percent in 2024 and slowly approach the ECB's 2 percent target by the end of the forecast period. As compared with the other founding countries of the euro area, inflation in Austria is expected to decline on a slower pace.

Demographic change will intensify shortages of labour force in the forecast horizon. However, as labour supply increases at a slightly slower rate than employment (+1 percent p.a.), this results in a decline in unemployment: the unemployment rate already fell below the pre-crisis level of 2019 in 2022 and is expected to reach 5.3 percent in 2027. This forecast assumes that as the working-age population declines, the existing potential for expanding labour supply can be realised, especially in the labour force participation of women and the elderly.

Despite extensive fiscal policy measures to cushion purchasing power loss due to high inflation, the budget deficit ratio will stabilise at around 1.5 percent of nominal GDP in the medium term. Public debt increases by 42 billion € over the forecast period. The debt ratio falls from almost 83 percent (2020: COVID-19 crisis) to just under 68½ percent (2027), mainly due to the strong expansion of nominal GDP.

Please contact

Further news