Iran War Threatens Economic Recovery

"The trends in crude oil and natural gas prices are crucial both for the inflation forecast and for the cost pressures expected by businesses. As the Iran war is triggering unpredictable price spikes, WIFO has decided to consider different price scenarios", says Marcus Scheiblecker, one of the authors of the latest WIFO Economic Outlook.

After two years of recession, Austria's GDP rose slightly again in 2025, by 0.6 percent. A marked pick-up in economic activity was particularly evident around the middle of the year, although this petered out again towards the end of the year. In the fourth quarter, domestic economic output stagnated.

The current uncertain international conditions are challenging a robust forecast. The future development of the Austrian economy will depend largely on how far crude oil and natural gas prices rise and how long they remain at high levels. This, however, depends on the unpredictable course of the war. WIFO has therefore decided to base its forecast for GDP and other key indicators on three scenarios:

- In the optimistic scenario, the Iran war lasts only a few weeks. The Gulf states' infrastructure for the extraction, processing, loading and transport of crude oil is not substantially damaged. The price of crude oil averages 80 $ per barrel until June and falls to 75 $ in the third quarter of 2026. The natural gas price – relevant to European electricity generation – averages 45 € per MWh until June 2026 and declines steadily after the end of the war.

- In the main scenario, the Iran war is also of short duration, but fossil fuel prices rise more sharply than in the optimistic scenario. After the war ends, prices gradually fall back.

- In the pessimistic scenario, hostilities in the Middle East continue until the end of the summer and destroy key infrastructure that must first be repaired. The crude oil price rises to 120 $ per barrel, remains at this high level until September 2026, and only falls below the 90 $ mark again in early 2027. The price of natural gas remains at 70 € per MWh until February 2027, as key production facilities have been destroyed, and gradually falls back by the end of the year.

In both the optimistic and the main scenarios, the economic recovery continues in the current year. In the optimistic scenario, economic output is expected to rise by 1.1 percent in 2026, and by 0.9 percent in the main scenario. In 2027, growth accelerates to 1.3 percent and 1.5 percent respectively. The pace of growth thus lags behind that of previous upturns.

In the pessimistic scenario, the moderate upturn observed so far is abruptly interrupted, resulting in GDP growing by just 0.2 percent in 2026 (2027 +0.4 percent). The high energy prices assumed in this scenario not only weigh on production and the real disposable income of private households, but also dampen business sentiment and consumer confidence. This results in an economic slowdown that goes beyond mere price effects.

In the main scenario, too, the renewed rise in inflation weighs on disposable incomes. As a result, private consumption continues to grow only modestly (2026 +0.5 percent, 2027 +0.6 percent). In the optimistic scenario, growth in the current year is somewhat livelier (+0.7 percent) and strengthens to 1 percent in 2027. In the pessimistic scenario, dampened consumer confidence – particularly heightened inflation expectations and unemployment – leads to a renewed rise in the savings rate. As a result, consumption barely grows in 2026 (+0.2 percent) and virtually stagnates in 2027 (+0.1 percent).

Government consumption expands by 1.2 percent in 2026 – only half as much as in the previous year due to the strained situation in public finances – and remains subdued in 2027 as well (+1 percent). It is assumed that the general government attempts in all three scenarios to stick to this expenditure path despite the savings target, so as not to place an additional burden on economic activity. The general government financial balance improves slightly in the main scenario to –4.1 percent (2026) and –4.0 percent (2027) of GDP (2025 –4.2 percent). In the pessimistic scenario, net lending amounts to –4.4 percent of economic output in 2026 and –4.9 percent in 2027 (without further measures; "No-policy-change" assumption).

The pronounced geopolitical uncertainty is most clearly reflected in domestic investment demand. In the main scenario, gross fixed capital formation rises by only 1.0 percent in 2026 (2025 +1.4 percent). It is not until 2027 that this component of demand will pick up pace again (+2.1 percent; optimistic scenario: 2026 +1.4 percent, 2027 +2.2 percent). In the pessimistic scenario, gross fixed capital formation contracts by 1 percent in the current year and does not grow again until 2027 (+0.8 percent).

The inflation forecast depends largely on assumptions regarding energy price trends. In the main scenario, the inflation rate falls to 2.7 percent in 2026 and further to 2.3 percent in 2027. In the pessimistic scenario, however, it rises to 4.1 percent and only eases to 3.5 percent in 2027. In the optimistic scenario, inflation stands at 2.5 percent in 2026 and 2.2 percent in 2027.

Despite the continued subdued economic performance, employment growth will gain momentum. In the main scenario, the rate of increase accelerates to 0.5 percent in 2026 and 0.8 percent in 2027 (optimistic scenario: +0.6 and +0.8 percent respectively; pessimistic scenario: +0.2 and +0.3 percent respectively).

In the optimistic scenario, the unemployment rate falls from 7.4 percent in the previous year to 7.3 percent, remains stable in the main scenario and rises slightly to 7.5 percent in the pessimistic scenario (2027: 7.0 to 7.6 percent).

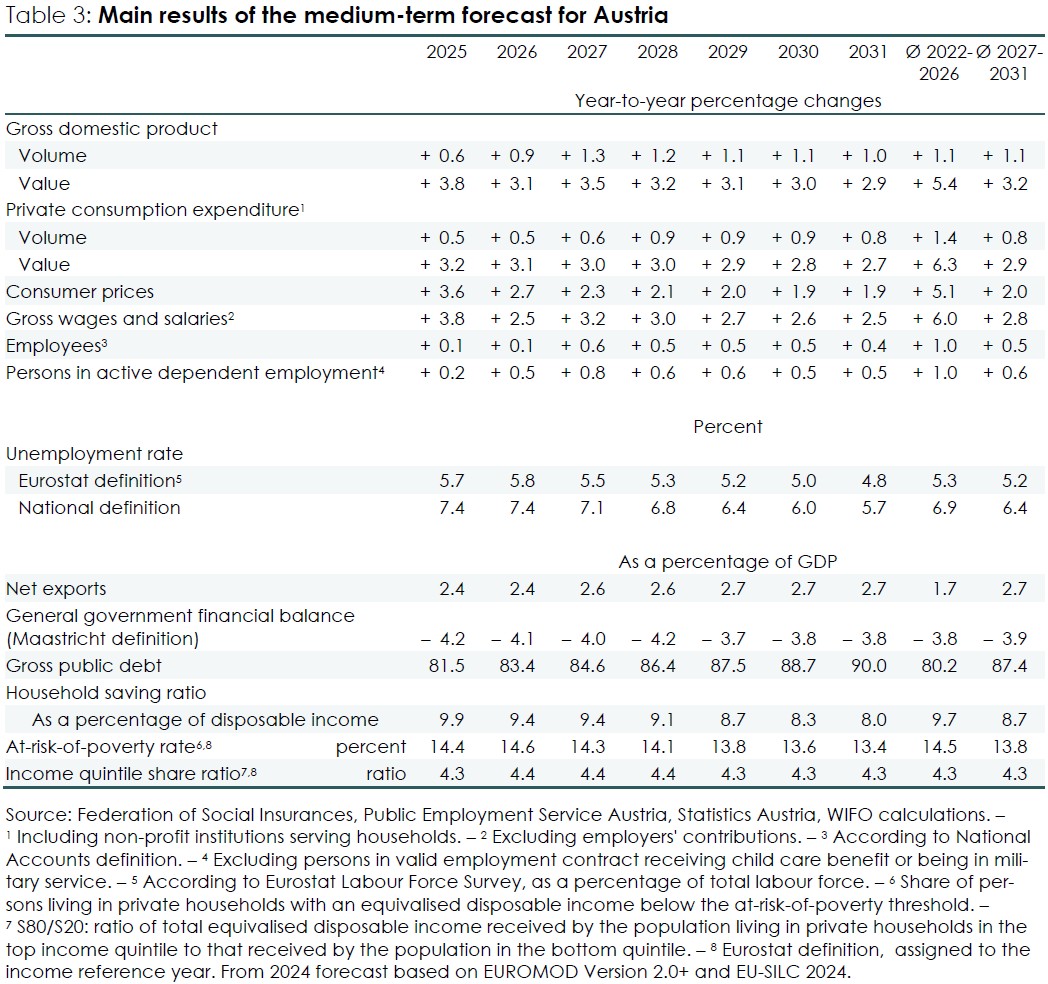

Medium-term Forecast

Building on the short-term forecast, WIFO projects economic developments for 2028-2031. This medium-term assessment is presented for the first time together with the short-term forecast at a press conference on 10 April 2026.

Publications

Please contact

Further news