Effects of the Corona Crisis on Public Budgets

The budget preparation in March was interrupted by the COVID 19 pandemic and the related measures in such a way that Minister of Finance Gernot Blümel himself pointed out that he had thrown out the originally planned budget speech.

A look into the Federal Financial Framework 2020 to 2023 published on 19 March 2020 shows that only a moderate decline in real GDP growth to 0.8 percent was initially forecasted for 2020. In the following years growth should recover to 1.4 percent respectively 1.3 percent in real terms. The Federal Medium-term Fiscal Framework published by the Federal Ministry of Finance only takes into account the first corona aid package of 4 billion €, which was adopted on 15 March 2020, and a decline in tax revenues of 1.3 billion € due to the cyclical downturn. Thus, a total deficit of –1 percent of GDP was projected for 2020 (in comparison, the WIFO forecast of December 2019 predicted a surplus of +0.3 percent). For 2020, the government programme also included slightly higher expenditures in some areas (environment, justice, home affairs).

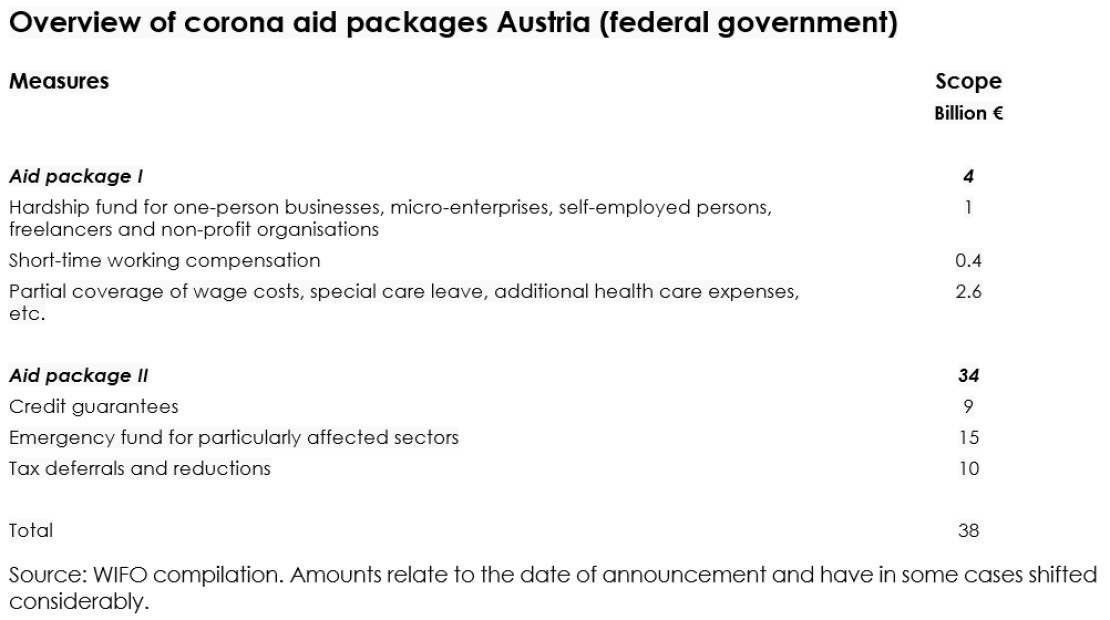

The budget path put forward by the Ministry of Finance underlying the Federal Medium-term Fiscal Framework is outdated in the meantime. Already on 19 March 2020, the federal government announced a further rescue package worth 34 billion €. Overall, the corona aid packages thus reach a potential maximum volume of 38 billion € (about 10 percent of the 2019 nominal GDP). At the same time, the government emphasised that it would provide further aid if necessary. Most of the Länder governments have also announced rescue measures, such as Tyrol (400 million €), Vorarlberg (100 million €) or Vienna (120 million €). Due to still incomplete information on the aid packages of the Länder, the focus of this analysis is on the federal measures.

First, it should be stressed that the starting conditions for coping with the budgetary consequences of the corona crisis in Austria are currently relatively favourable. Since 2018, the general government balance has been positive; a Maastricht surplus of 0.3 percent of GDP was originally expected for 2020. The debt ratio, which peaked in 2015 at around 85 percent of GDP after the financial and economic crisis, was expected to fall to around 67 percent by 2020. The financing conditions for the necessary new debt are historically favourable: two days after the announcement of the aid packages, the yield on ten-year bonds was 0.185 percent, which is below the average of the past five years. It can therefore still be assumed that the necessary higher debt levels resulting from the measures adopted will not be reflected in worsening financing conditions.

Measures to tackle the corona crisis have different effects on the government balance. Loan guarantees and credit liabilities only burden the budget in the event of an actual loan default. Reduced tax revenues due to reduced advance tax payments are directly relevant for the budget this year. In contrast, the deferral of social security contributions will not worsen the Maastricht balance, but only the final default. The projected budgetary effects are therefore strongly driven by assumptions about the design and utilisation of the crisis management packages, which have not yet been fully specified at this stage.

In the WIFO macroeconomic scenario of 26 March 2020, the effects of the federal aid packages on expenditures are assumed to amount to approximately 12½ billion €. This figure includes emergency aid and investments to support the healthcare system, in part also for the police and the armed forces, as well as expenditures for charitable organisations. The originally set budgetary ceiling of 400 million € for financing the short-time working model will probably be significantly exceeded, and expenditures of 1 billion € are assumed. There is particular uncertainty as to whether the liquidity of the corporate sector will be secured by direct support payments or by loan guarantees from the state. Regarding the currently discussed liability shares of 80 percent, it must be considered that a guarantee that is below 100 percent means that the banks bear part of the default risk. This provides the right incentives, but also entails the need for checks, which could jeopardise the urgently needed short-term provision of liquidity. The emergency aid of around 6 billion € estimated in the budget scenario is intended to cushion losses in turnover and to support small and medium-sized enterprises that are particularly affected by official closures.

In addition to these measures, automatic stabilisers operate, which help to cushion cyclical fluctuations. On the revenue side, this will be reflected in lower revenues from corporate income tax and assessed income tax. The extent to which employment is stabilised by short-time working and business support measures will play a role in the development of wage tax and social security contribution revenues. This clearly shows a trade-off for economic policy: the corona-short-time working model entails high direct fiscal costs if it is heavily utilised. At the same time, the model supports revenues from wage tax, social security contributions and VAT via private consumption. Furthermore, revenues from other taxes and levies – in particular from indirect taxes such as the excise tax on mineral oil, the family equalisation fund (FLAF) and the tax on wage sum (Kommunalsteuer), but also from capital gains tax – as well as dividend income and production revenues of the state are falling. In this scenario, net lending or borrowing deteriorates to –21½ billion € or –5½ percent of GDP, and government debt is assumed to increase to around 76 percent of GDP.

An assessment of the Austrian aid package in an international comparison is only possible to a limited extent because the measures vary from country to country, also regarding their budgetary effects. However, all aid packages announced so far have in common that they include a mix of tax relief (tax deferrals or tax reductions) as well as direct support payments and credit guarantees for companies. The main objective of the aid measures is to prevent mass corporate insolvencies and unemployment as a result of the epidemiological measures to slow the spread of the virus, which are causing massive declines in turnover in several sectors. There are also indications that many countries intend to implement very extensive packages of measures, even compared to the economic stimulus packages implemented to cushion the effects of the recent financial and economic crisis. In general, governments are demonstrating their determination to do "whatever it takes" to limit the real economic effects of the crisis by trying to bridge liquidity bottlenecks in companies and avoid layoffs, e.g. through short-time working.

Germany has adopted a protective shield of 1.2 trillion € (35 percent of GDP); the Maastricht deficit is currently forecasted at 4.5 percent of GDP. The German aid package includes a supplementary budget of 156 billion € (additional expenditure of 122.5 billion €, including 50 billion € in emergency aid for the self-employed and SMEs, 10 billion € in short-time work, higher healthcare expenditure, continued wage payments for a maximum of 6 weeks for employees with children under 12 years of age with care obligations; tax shortfalls of 33.5 billion €) and an "Economic Stabilization Fund" of 600 billion € for all companies (of which 400 billion € guarantees to secure corporate liabilities, 100 billion € for direct temporary equity investments in enterprises and 100 billion € borrowing to refinance KfW's corona-related special programmes). In addition, the guarantee framework for KfW will be extended to a maximum of 449 billion €. The UK has adopted an aid package of 350 billion £ (just under 16 percent of GDP), of which 20 billion £ take the form of tax cuts and non-repayable loans for SMEs and 330 billion £ are loan guarantees. The four largest EU countries, Germany, France, Spain and Italy, intend to implement fiscal measures (expenditure increases and tax cuts) averaging about 1 percent of GDP and guarantees of about 14 percent of GDP.

The EU itself has launched an "investment initiative to tackle the corona crisis", which will redirect 37 billion € of unused and unallocated structural funds. In addition, the scope of the European Solidarity Fund will be extended so that the 800 million € available for 2020 can be distributed to affected member countries not only in the event of natural disasters but also for health crises. A further 179 million € can be used from the European Globalisation Fund to support the unemployed in the event of a crisis. Thus, a total of up to 38 billion € (just under 0.3 percent of EU GDP) is available. The IMF provides aid of up to 1 trillion $, including 50 billion $ in emergency loans for emerging and developing countries, of which 10 billion $ will be provided at zero interest.

Please contact

Further news