Weekly WIFO Economic Index

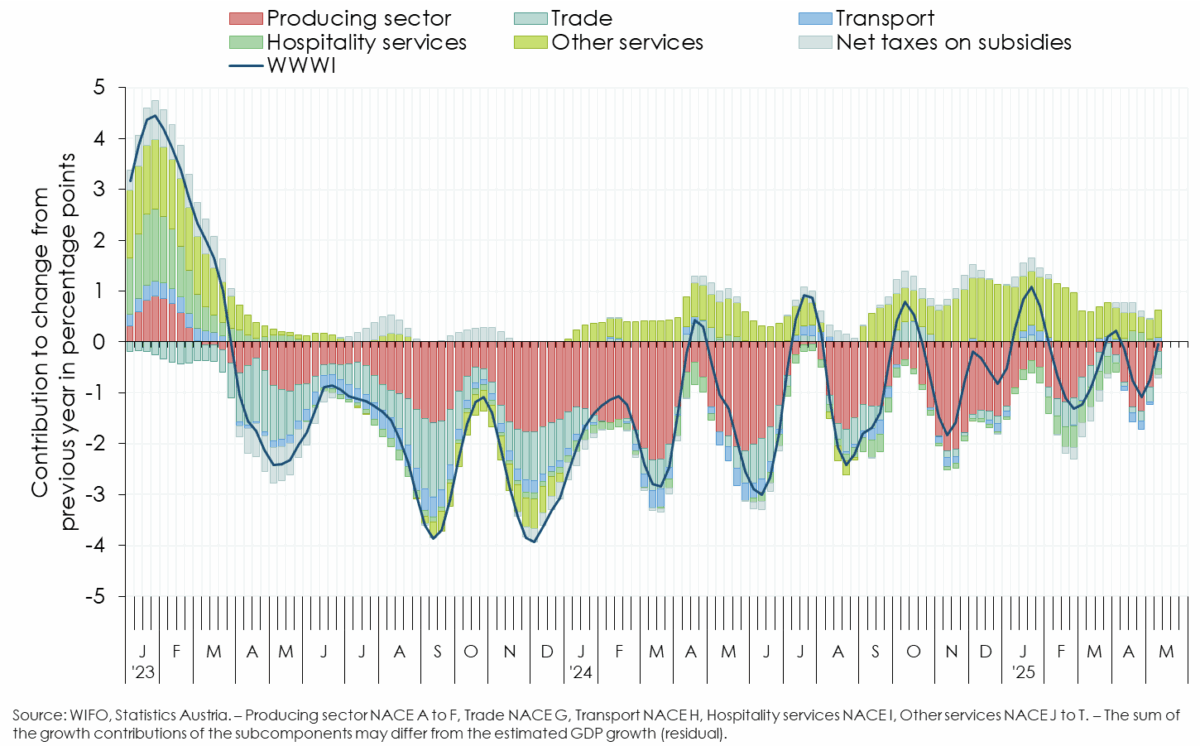

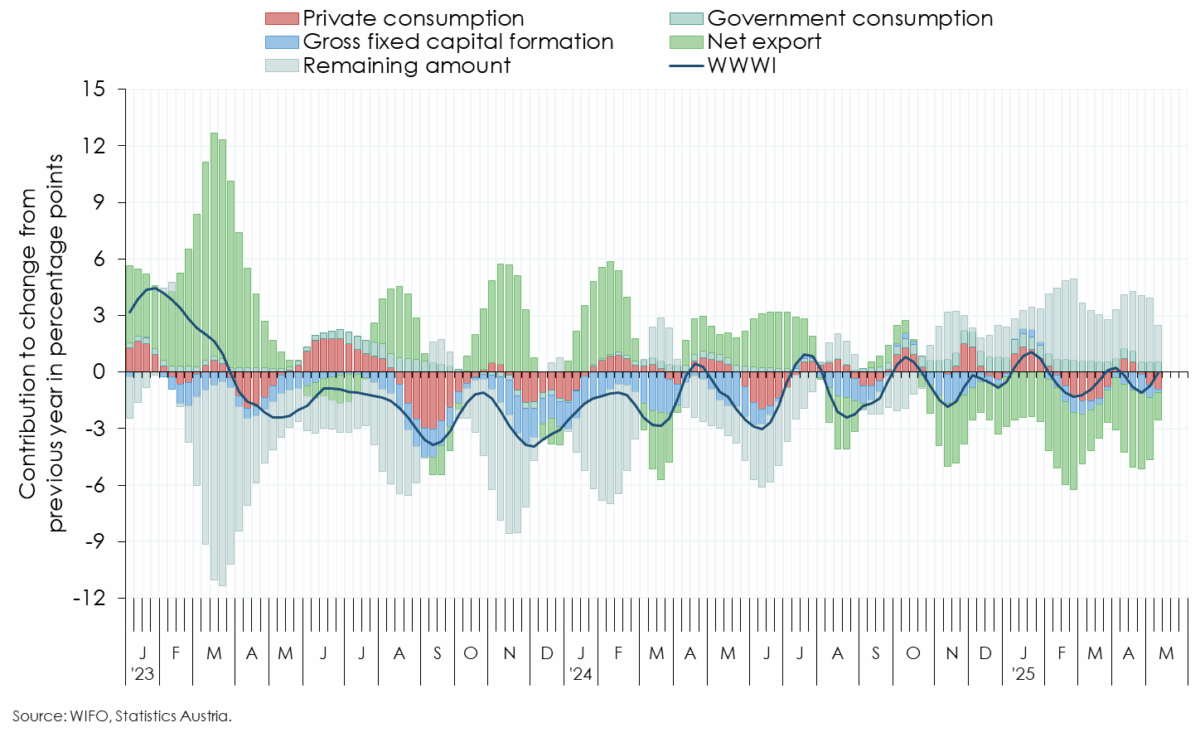

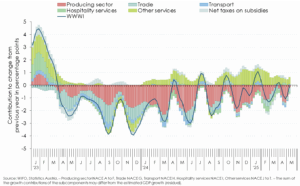

WWWI for GDP and its subcomponents

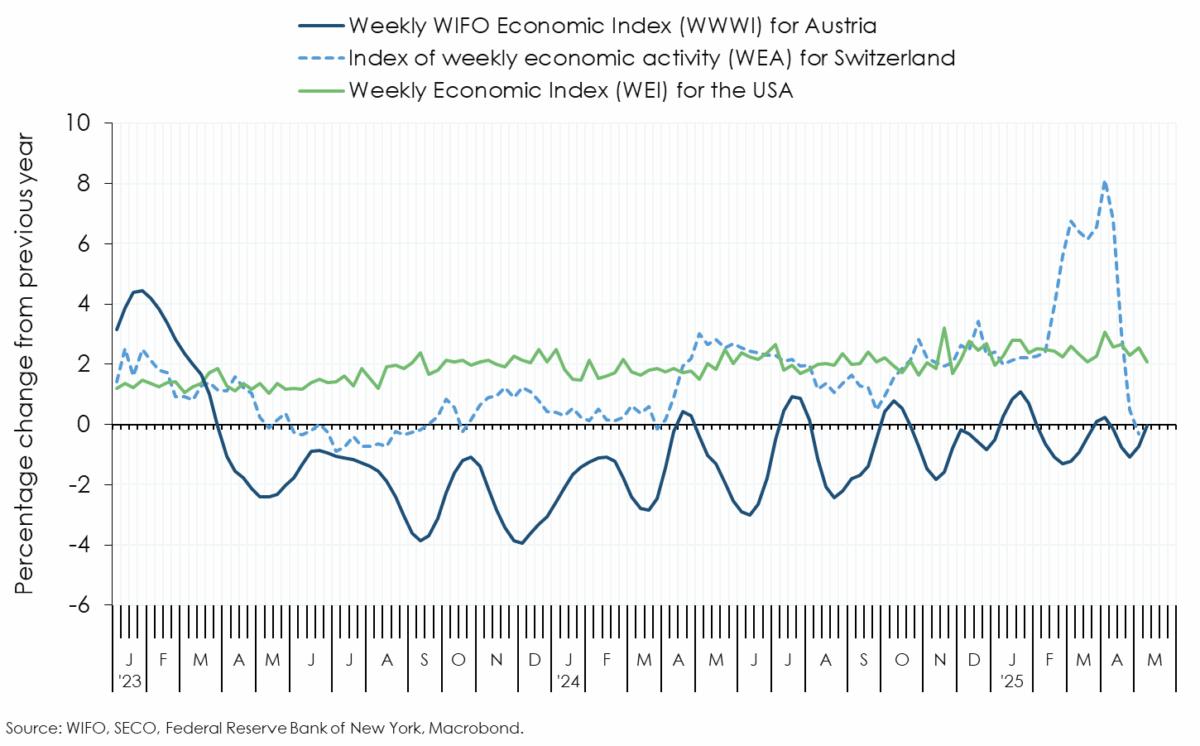

Based on the weekly GDP indicator (WWWI), domestic economic output in April and the first two weeks of May was ½ percent below the previous year's level, as it was in March (revised)1. Due to the seasonal shift of Easter – with Holy Week and thus the Easter holidays falling in the last week of March in 2024 and the third week of April in 2025 – there was a significant year-on-year increase in tourism in April, especially in services consumed by private households. In contrast, the goods-producing sector (industry and construction) likely performed more weakly in April than in March and May.

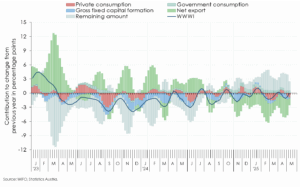

The inflation-adjusted volume of non-cash transactions, as an indicator of household consumption expenditure, shows a slight increase in demand for goods (retail sales) and a stronger increase in demand for services compared with the previous year in April. In the first half of May, demand for goods and services likely declined at a similar rate. Private consumption is therefore expected to have been ½ percent higher in April and 1½ percent lower in the first half of May than in the same period last year (March –2½ percent).

The development of gross fixed capital formation is determined by estimated economic output (industrial production) and sentiment in the manufacturing sector, as measured by the WIFO-Konjunkturtest (business cycle survey). In April, investments are expected to have been 3 percent lower than in the previous year (March –1¾ percent).

Developments in industrial production and tourism, as well as in the main components of demand and the resulting effects on foreign trade, resulted in net exports contributing negatively to GDP growth by 3½ percentage points in April (March –2 percentage points).

The number of trucks on Austria's motorways and rail freight traffic declined in April compared to the previous year. Conversely, the number of passenger flights and the volume of freight handled at Vienna Airport increased. According to the WIFO-Konjunkturtest, the majority of companies in the transport sector continue to assess their current business situation as negative, despite a tendency towards improvement. Based on these indicators, value added in the transport sector (NACE 2008, section H) is expected to have declined by 2 percent year-on-year in April (March +1 percent, first half of May +½ percent).

Employment in the goods-producing sector (NACE 2008, sections A to E) has continued to decline due to the recession, with the number of job seekers rising at double-digit rates year-on-year since November 2023. Although the WIFO-Konjunkturtest indicates a slight improvement in both the assessment of the current situation and the expectations for the coming months, sentiment remains far in negative territory. WIFO expects economic output in the goods-producing sector to have been 4 percent lower in April than in in the previous year (March –2¼ percent, first half of May –2 percent)2.

Sentiment among construction companies is not yet showing signs of sustained improvement. Following temporary declines at the beginning of the year, the number of people registered as unemployed in the construction sector increased slightly again in April. Employment also fell somewhat more sharply. Value added in construction (NACE 2008, section F) is estimated to have been 3¼ percent lower in April than in the same period of the previous year (March +1½ percent, first half of May –2½ percent).

Based on cashless transactions in the restaurant and hotel sector, as well as sentiment indicators from the WIFO-Konjunkturtest, value added in tourism (accommodation and food services, NACE 2008, section I) is estimated to have been 2½ percent higher in March than in the same period of the previous year (March –9 percent, first half of May –1 percent). This increase is due to the timing of Easter: in 2024, the Easter holidays fell in calendar week 13, i.e. in March, whereas this year they fell in calendar week 16, i.e. in April. Value added in the wholesale and retail trade sector (NACE 2008, section G) is estimated to have fallen by 1¼ percent year-on-year in April. Compared with March (–3¾ percent) and the first half of May (–3 percent), there was also a slight seasonal Easter effect in trade on a year-on-year basis.

The current employment situation in the remaining market services and sentiment indicators from the WIFO-Konjunkturtest suggest stagnation in this sector. Value added in the remaining market services (NACE 2008, sections J to N) is expected to have remained at the previous year's level in April (March +½ percent, first half of May +¼ percent). Based on price-adjusted non-cash payments in the entertainment sector, value added in other personal services (NACE 2008, sections R to T) value added is estimated to have been ¼ percent lower in April than a year earlier, as in March (first half of May –2¼ percent).

1 The inclusion of newly published monthly and quarterly data, which must be taken into account when estimating the WWWI, led to a revision of the WWWI. For March, notable downward revisions on the production side occurred in particular in trade (NACE 2008, section G) and the remaining market-related services (sections J to N). Larger upward revisions had to be made for the construction sector (sections F).

2 The WWWI estimates are modelled using unadjusted weekly and monthly data compared to the previous year. The calculations are therefore affected by ½ working day less in April and one working day more in May than in the previous year, particularly in the goods producing sector and the closely related market services and construction.

Weekly Economic Activity, WWWI – Production, WWWI – Demand The WWWI is under constant development; it is regularly reviewed and will be expanded with new and additional weekly data series as they become available. The WWWI is not an official quarterly esti-mate, forecast or similar of WIFO.

The WIFO Weekly Economic Index (WWWI) is a measure of the real economic activity of the Austrian economy on a weekly and monthly frequency. It is based on weekly, monthly and quarterly time series to estimate weekly and monthly indicators for real GDP and 18 GDP sub-aggregates (use side 8, production side 10) of the Quarterly National Accounts.

With the release for June 2022, the econometric models for the historical decompositions and for nowcasting have been converted to seasonally unadjusted time series. In addition, year-on-year growth rates are now used to estimate the models.

The WWWI estimates are (currently) updated monthly and published on the WIFO website.

Please contact

Further news